By Kalim Siddiqui

I. Introduction

Capitalism may be defined as an economic system based on the private ownership of the means of production, and the owners of capital aim to maximise their profits. Mainstream economists believe that capitalism is the most efficient and productive system, and private property promotes efficiency by giving the owner of resources an incentive to maximise their value. It is assumed that the markets are perfectly competitive in an ideal situation, with the possibility of free entry and exit. The producers are price takers, and no one has the power to influence the price. Adam Smith (1776) argued that all economic agents must be allowed to pursue their self-interest without any hindrance.

Mainstream economists emphasise the virtues of competitive markets, market efficiency, consumers’ sovereignty, and rationality. However, perfectly competitive markets do not hold in the real world, and there are externalities such as increasing returns to scale, asymmetric information, and imperfect competition. The real world is far from the ideal world. There is little doubt that the very animal spirit that has been the defining feature of the capitalist process has devastated nature, depleted fossil fuels, and is responsible for climate change, soil erosion, and sharply widened global inequality between nations (Saad-Filho, 2010; Siddiqui, 2019a; Steward, 1995).

Capitalism is essentially a money-using economy where money is used to make transactions. Some people decide to use money as a form of wealth, not using it immediately but holding it for some time (Armstrong and Siddiqui, 2019). I mean, if people decide to hold money, that means they will not spend on buying goods, and that would lead to a shortage of demand for goods. There would then be under-capacity utilisation, a rise in unsold stocks and unemployment, and a fall in output. This is called an overproduction crisis. This problem was overcome by external markets, which means colonial markets were necessary for the development of capitalism (Siddiqui, 2021b; also, 2018a).

Political economists attempt to include economic analysis with policies on the ground and view economic activity in a political context. This view is concerned with the relationship between economics and politics, emphasising the role of power in economic decision-making (Siddiqui, 2021f).

There have also been suggestions by mainstream economists and international financial institutions that post-colonial countries should increase the production of primary commodities. By exporting such commodities, they could earn foreign exchange to finance technology imports and speed up their industrialisation. However, an increase in the supply of primary commodities could bring down prices in export markets. The terms of trade between primary commodities and manufacturing moved against the former for a long period after the Second World War (Siddiqui, 2018a; also, 2018e).

At present, most developing countries export a handful of primary commodities, and an increased supply of primary goods would lead to a collapse in the prices of these goods. Moreover, the raw-material prices were kept down by income deflation during the colonial period (Siddiqui, 2020c; also, 1990a), but at present, it is done through globalisation and austerity policies.

The growth of finance requires price stability. But we have seen that the growth of the economy created an expansion of finance (Siddiqui, 2020b; also, 2019a). For instance, as the leading economy in capitalist countries, the US has run a current account deficit since the 1990s. US military expenditure has risen sharply due to its involvement in several wars and maintaining more than 230 military bases worldwide. The country pays this current account deficit by simply printing dollars. However, before 1913, when Britain was the leader of the capitalist world, the country did not settle the current account deficit by printing pounds sterling. Still, it settled the deficit by the colonial “tribute” (also known as “drain”). Britain claimed the export incomes earned by the colonies to settle its current account deficit with then-emerging economies of Western Europe and the US. But at present, the US has no such colonies, and when the US prints dollars, those who hold it could claim it, so that the US becomes indebted to those countries and individuals who hold it (Siddiqui, 2020d; also, 2019b).

We need to present a logical critique of Eurocentric interpretations of economic history, i.e., relations between colonisers and colonised, which resulted in uneven accumulation and impoverishment of the masses in the colonies. Inconsistent development results from many factors, including primarily the past imperial domination. This created the co-presence of a modern sector (usually controlled by foreign companies) and a traditional sector characterised by the pre-capitalist mode of production, which is dominated by merchant and feudal elites. The accumulated capital is diverted into activities such as speculation, money lending, real estate, and hoarding, rather than investment in the modern industrial sector.

Britain was the country that pioneered the industrial revolution, starting with the cotton textiles industry. However, Britain did not grow any raw cotton. The industrially pioneering country would need control over distant tropical and semi-tropical lands that could produce natural cotton, and to get them to supply the quantities it required (Siddiqui, 2018c; also 2016). Thus, once we move away from the fairytale of “free trade” occurring by “factor endowments” in a situation where the factor endowments themselves were supposedly frozen and could not migrate across country borders, then “imperialism” becomes impossible to ignore. Mainstream economists do precisely this; they forget imperialism and explain trade resulting from capital and labour not being traded or relocated.

In the United States, the first finance minister, Alexander Hamilton, in his report on manufacturing submitted to the US Congress in 1791, after the country became independent, pointed out that a backward country like the US should protect its industry in its “infancy”. According to him, if the US wanted to modernise and become a strong nation, it needed to establish industries through import tariffs. This is what the US government did, keeping a high tariff of around 45-50 per cent between 1800 and 1913. And during the Great Depression in 1930, it introduced the Smoot-Hawley Act, which raised tariffs even higher. Thus, with the help of these protectionist policies, the US managed to build industries.

Another successful example of industrialisation was Japan after the Second World War. In studying Japan’s post-war economy, Johnson (1995) stressed the centrality of the state’s role in successful economic development, particularly that of Japan and East Asian countries. Furthermore, a few studies have also underlined key features such as planning, relative state autonomy, bureaucratic coordination, the private concentration of big conglomerates, the exploitation of the female workforce, and low expenditures on social welfare (Cummings, 1987). It did not adopt a neoliberal policy to facilitate industrialisation. Rather than keeping import duties high, the government controlled imports through foreign exchange regulation. Exports were promoted to earn the foreign exchange needed to import high tech from abroad. The domestic industries operated in a competitive environment and were encouraged to achieve efficiency and reduce costs. The government created the MITI (Ministry for Industrial Trade and Industry) to facilitate domestic industrialisation. A directed credit programme did this by subsidising sectors.

Moreover, Japan in the 1950s barred foreign investment in key industries. Foreign companies were required to transfer technology and had to buy specific proportions of inputs locally. Foreign ownership was restricted to a maximum of 49 per cent. For example, Toyota Automobile started as a textile machinery manufacturer and moved into car production in 1933. The Japanese government kicked out General Motors and Ford in 1939 and, with its own money, bailed out Toyota. After twenty-five years of trying, it slowly established itself as a car manufacturer. Today, Toyota has become the world’s most efficient car producer, and its luxury brand Lexus has become an icon for globalisation (Siddiqui, 2015a; also 2015b; Johnson, 1995).

However, for the last three decades, since the Plaza Accord, and with the upsurge of global capital liberalisation, Japan’s growth has stalled, resulting in the revaluation of the yen. This affected export competitiveness and productive investment. And with financial liberalisation, the banks are no longer the instrument of industrial policy, as was the case during the post-war period. On the Japanese economy, the London-based Economist (2021, December 11) commented: “Overall growth has remained sluggish, but growth per head has recently been higher than others in the G7. Unemployment has been minimal; longevity has increased, and inequality has stayed relatively low.”

The US and its allies created the IMF (International Monetary Fund) and World Bank at Bretton Woods in 1944. Both organisations were to pursue a dirigiste economic strategy. Keynes advocated supporting the dirigiste strategy and focusing on expanding domestic markets. However, in the 1980s, with the global slowdown in growth rates and the debt crisis leading to a balance of payments crisis in most developing countries, the IMF was ready to lend money to stabilise their economies. But these countries had to adopt market reforms known as “Structural Adjustment Programmes” (SAP), also known as “Washington Consensus”, until their economies experienced a balance of payment deficit. These policies included dismantling all import and capital controls, privatisation of public sector assets, cuts in social spending on health and education, and introducing “labour market flexibility”. Recent records show that the IMF forced these countries to undo earlier policies of the dirigiste regime and facilitate neoliberal reforms. It seems that the IMF is an instrument for ushering in a neoliberal regime and promotes the interests of global financial capital.

Under neoliberal globalisation, since the collapse of the Soviet Union in 1991 and the integration of the East European economies with the EU, monopoly-finance capitalism has escalated drain from the peripheries but with declining relief to their domestic workers, which coincided with the decline of trade unions’ role in wage bargaining. Furthermore, the US-led advanced capitalist countries have continued to escalate their intervention in internal affairs and create insurgencies such as situations in the peripheries that justify military intervention. This period has also been accompanied by accelerated rural exodus, a sharp rise in the informal sector, and unemployment in the peripheries.

The US has intervened directly or indirectly in most of the developing countries since the Second World War, for economic and strategic interests. A closer look at US intervention shows us that it has not only intervened but also used various forms of intervention. Besides intervening directly by using force on a large scale, the US has also sent military advisers and weapons to interfere in the internal affairs of developing countries (Siddiqui, 1990b).

US interventions seem to be motivated by economic interests, i.e., controlling raw materials, export markets, and foreign investment. For instance, the US carried out an economic blockade against Allendeʼs elected government in Chile in the early 1970s, which focused on the termination of all US economic assistance, and no loans from the World Bank, IMF, and Inter-American Development Bank to the Allende government. The US refused to renegotiate Chileʼs external debt to the US, most of which was accumulated in the 1960s under the Alessandri and Frei regimes. The continuing process of escalating economic warfare and covert subversion deepened the crisis in the Allende government, paralysed the economy, provoked social disorder, created instability and promoted the conditions for a military coup in Chile in 1973.

In Iran in 1953, funds were provided by the CIA and the UK intelligence services to plot a coup d’état that overthrew the government of Prime Minister Mosaddeq. The UK had controlled Iranʼs oil for decades through its Anglo-Iranian Oil Co. After months of talks, Mosaddeq broke off negotiations and denied the UK any further involvement in Iranʼs oil industry. Soon after, the UK and the US planned to overthrow Mosaddeqʼs government and restore power to the Shah of Iran. Mosaddeq was placed on trial and spent the rest of his life under house arrest until his death in 1967. The Shah was brought by the US and ruled Iran for another twenty-five years until the 1979 Iranian Revolution.

The US has intervened in the internal affairs of Haiti (1915-34), Guatemala (1954), Korea (1950-3), Vietnam (1961-73), Cuba (1961) to remove Fidel Castro, Indonesia (1965), Congo (1960-8) to remove Patrice Lumumba (the first legally elected prime minister of the Congo, assassinated by the CIA in 1961), Ecuador (1963, 1981, 2013), Chile (1970-3), Pakistan (1977-9) to remove Z.A. Bhutto (executed in 1979), Nicaragua (1978-9), El Salvador (1979-89), Brazil (1980), Lebanon (1981-4), Grenada (1983), Panama (1989), Venezuela (2002), Afghanistan (2001-21), Iraq (2003-11), and many more (Siddiqui, 2013; also 1990b).

II. Colonies and the Development of Capitalism

The development of capitalism in Western Europe coincided with colonial expansion and the occupation of vast territories of the world. Imperialism existed during the colonial period and persists even today. The later stage of capitalism, imperialism, increasingly relies on monopoly, not competition, and accumulation by dispossession for its survival (Siddiqui, 2018f).

Historically, the rise of capitalism in Britain began with the most brutal forms of “primitive accumulation”, including, domestically, dispossessing serfs of their land by lords, also known as “the Enclosure Movements”, and, externally, by transporting of millions of enslaved Africans, colonial plunders, deindustrialisation in the colonies, repeated famines, and deflation of incomes of people in the colonies to keep raw-material prices down, and opium trafficking (Siddiqui, 2020a; also, 2020b). The common land that had been at the disposal of peasants and serfs for grazing by the village livestock and for other purposes was reclaimed by the lords, in England in the period from 1750 to 1860. This was carried out in the name of improving agricultural productivity.

There is a prevailing myth that the advanced capitalist countries, such as Britain, owed their prosperity and economic development to the policies of “free market”, “free trade”, and balanced budgets. However, the real facts are otherwise. Protectionist policies to develop industry were initiated by the first British Prime Minister, Robert Walpole (1721-42), and continued until the middle of the nineteenth century. This helped British industries to establish themselves. To promote its cotton industries, Britain banned cotton textile imports from India, destroyed the Irish woollen industry and banned the development of high-technology products in the colonies (Siddiqui, 2021d; also, 2018e).

Britain’s aim was that colonies should produce primary commodities to supply raw materials at low costs to British industries. Once British manufacturing became internationally competitive, Britain adopted a “free trade” policy, since it was in her interest. Moreover, by the second half of the eighteenth century in Western Europe, especially in England, the growth of manufacturing and industrialisation broke the vicious circle of diminishing returns. Increasing returns (i.e., economies of scale) meant that, as production expanded, the cost of production per unit fell. Increasing returns combined with a division of labour led to rising productivity.

From the second half of the eighteenth century, Britain’s economic policy with its colonies was based on simple economic principles, i.e., importing raw materials and exporting industrial goods. For successful industrialisation, a key requirement was the initial protection of domestic industries, acquiring a cheap supply of raw materials and increasing returns. Afterwards, an expanding market was vital for manufactured goods to be sold. And thus, external markets have been and still are very important for capitalism. Trade rose following enhanced British manufacturing competitiveness with the Industrial Revolution in the second half of the eighteenth century.

As an example, during the British colonial period, population growth in India was negligible due to the high mortality rate, low incomes, and repeated famines. Moreover, availability of foodgrain per capita declined as more land was devoted to cultivating commercial crops. Colonialism squeezed people’s consumption to take away commodities that Britain needed (Sen, 1981; Siddiqui, 2020b).

The Industrial Revolution began with cotton textiles in Britain, but raw cotton did not grow in Britain, which meant that cotton and other raw materials had to be imported. However, Britain did not make substantial investments to cultivate commercial crops in colonies like India, and the land under cultivation of commercial crops increased the cost of foodgrain crops. As a result, land used to grow foodgrain was reduced, and famines became a repeated occurrence under the British colonial regime in India. The data shows that the availability of foodgrain per capita witnessed a steady decline in India during the colonial period (Siddiqui, 2020b).

The role of Britainʼs colonial markets (external markets) started to become important in the second half of the eighteenth century. Karl Marx was aware of it, but he did not make this issue a major part of his study. Marx, in Das Kapital, focused in detail on the origin of surplus value, and the relationship of capitalism with the colonies did not enter Marx’s economic analysis, although he did mention the phenomenon in passing. However, later, Rosa Luxemburg and Lenin took up the role of the market. The colonies provided two crucial things for Britain, namely the availability of external markets and the supply of cheap raw materials. Britain sold its manufactured goods in the colonies, which caused the destruction of local handicrafts, and local craftsmen lost jobs and had to rely on agriculture. Thus, increasing the pressure of the population on the land, under circumstances where the state undertook no additional investment, resulted in a whole range of phenomena such as overcrowded agriculture, high rents, a rise in farmers’ debts, and low wages.

III. Periods of Capitalism

The history of capitalism tells us the necessity of the accumulation of wealth and, historically, can be divided into five periods.

The first period of capitalism began with the European powersʼ colonisation of most parts of Asia, Africa, and Latin America. Britain was the first nation where industrialisation started, gradually in the second half of the eighteenth century. As a leading capitalist country, Britain had the biggest empire until the First World War, which was marked by the existence of the gold standard.

From the colonies, mainly raw materials and primary commodities were exported to Europe and North America, and colonies had a trade surplus with these countries. In contrast, Britain had a balance of payments deficit with Europe and North America. The irony is that Britain not only paid off her trade deficits from the coloniesʼ trade surplus, but also exported capital to the then-emerging economies of Europe and North America. Britain was charging the colonies between 3 and 6 per cent of the country’s GDP as a tribute for governing them, which Britain got free to settle its balance of payments deficit with the then-emerging industrial countryside, the US, the Netherlands, and Germany.

The question arises: how was this possible? This was also a phase when capitalism had a long economic boom from 1860 to 1913. This ended with the First World War, for several reasons, including that the colonial market where Britain was selling its goods became exhausted, mainly because the incomes of the masses in the colonies were not growing.

The second period of capitalism started after the First World War and continued up to the inter-war period. In fact, after that war, Britain went from being a leading creditor nation to a debtor nation. The economic performance of the industrialising countries, such as Germany, Japan, and the US, was better than that of Britain during the inter-war period. They were selling cheaper goods in the colonial markets. Britain was no longer able to sustain its position within the gold standard.

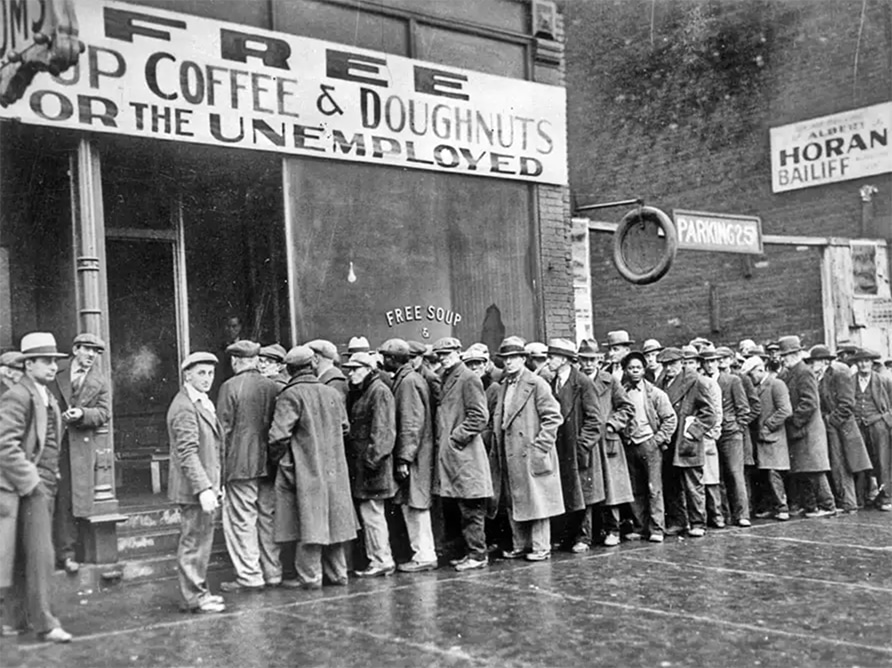

The Great Depression began in the 1930s because of an overproduction crisis and problems with unsold goods, resulting in mass unemployment in industrialised countries. Economic historian Charles Kindleberger (1978) noted that the Great Depression of the 1930s took place because Britain could not sustain its world leadership role. According to him, capitalism is an international system and requires a leader. Britainʼs global role as a leader was declining, while the US was not yet able to assume that role. However, S.B. Saul, a British economic historian, acknowledged the important part of the colonies in providing markets. He said that colonies provided a “market on tap”, and Britain could dump anything in the colonies.

Karl Marx (1973) criticised J.B. Say’s law that ‘supply will create its own demand’. Marx highlighted the demand problem. The problem of aggregate demand led to ‘realisation crises’. About five decades later, Keynes saw an overproduction crisis. Say’s law rejected the possibility of a deficiency of aggregate demand. Aggregate demand may be deficient due to increasing inequality, and this inadequate demand would undermine profits and investments and, thus, the overall growth rates of the economy (Keynes, 1930).

The third period of capitalism came about soon after 1945 and continued until the late1960s, also known as the post-war boom period. For more than two decades, major capitalist countries saw a rise in investment, low unemployment, steady GDP growth, and a substantial increase in labour productivity and wages. This was a period when trade unions were seen as an important element in wage negotiation disputes, and the government took various measures to improve workers’ welfare and working conditions. This is known as the “Golden Age” of capitalism, made possible through state-initiated aggregate demand management.

The British economist John Maynard Keynes (1930) analysed the economic crisis during the inter-war period and suggested that the state could play a role in expanding the market. He contended that the massive persistent unemployment in the advanced capitalist countries during the Great Depression made it clear that the free market was not self-regulating. It would be stupid to wait for a long period for the economy’s self-correcting mechanism to eliminate such unemployment. However, his ideas were not then taken seriously by the British government.

According to Keynes, the state could enlarge the market so that capitalism could get rid of the overproduction crisis. However, his suggestion of demand management was taken more seriously only after the Second World War, when the state became involved in a big way by using fiscal policy both in Europe and in the US as a market for goods, and state expenditure rose as a proportion of GDP in all the industrialised countries. Keynes stated that demand management would not work to save capitalism, and a somewhat more comprehensive “socialisation of investment” would be necessary after a period. It was assumed that public spending, especially on infrastructure, would have a magnified impact through the multiplier. The initial beneficiaries of government expenditure would spend their income, thereby increasing the revenues of others in society. Keynes thought that the new activist government would be a more humane form of capitalism (Keynes, 1930).

The fourth period of capitalism began in the late 1960s and continued until 1980. In fact, after the Second World War, colonies began to achieve political independence, and the prices of raw materials could not be directly depressed, as happened during the colonial period. As a result, rising costs of raw materials and primary commodities, including oil, brought rapid inflation in 1973 in the industrialised countries. Capitalism again faced a deep and prolonged crisis, and the “Golden Age” was unsustainable.

During the 1973 oil crisis, this became more obvious, when oil prices rose sharply. The advanced capitalist countries experienced stagflation as prices and unemployment rose to high levels compared to previous decades. To solve the crisis, they adopted neoliberal policy and, from the mid-1970s, combating inflation became a key priority policy for these countries, rather than unemployment.

During the anti-colonial struggle in India, it was said that the living conditions of the masses would be improved after independence, and foodgrain production would be increased to avoid famines and meet the foodgrain demands of the rising population (Siddiqui, 2020b; also, 2019a). It was said that, through land reforms and public investment in irrigation, rural infrastructure, and power, foodgrain output would be increased, and rural equality would also be achieved. Meanwhile, the increase in foodgrain production was supposed to keep inflationary pressure down and save the country from foodgrain imports.

In post-independent India, the state purchased farmersʼ crops at remunerative prices and subsidised power, water, and credits to increase farmersʼ output and income. The state also undertook substantial investment in irrigation works and research and development of new seeds to help farmers raise their incomes (Siddiqui, 2021a; also, 2018e).

If raw-material prices rise and product prices and wages remain the same, profits will be reduced. Therefore, businesses will do everything to depress the prices of raw materials. Furthermore, developing countries are told to adopt austerity measures during inflation. At the same time, interest rates are raised to reduce demand and reduce state expenditure. The overall market is squeezed, which results in income deflation.

Joseph Schumpeter (1976) said that the key elements in the dynamism of capitalism reside in the notions of entrepreneurship and innovation. According to him, the entrepreneur is the main actor, driven by the profit motive, and it is the entrepreneurs who arrange finance and combine factors of production to produce the final products. Schumpeter also mentioned that there is a process of “creative destruction”, where a new approach in methods of production is adopted, and the old one is constantly discarded.

The fifth period of capitalism is the prevailing protracted crisis in the advanced capitalist countries. They have adopted increased global market integration, capital and trade liberalisation, and further concessions to multinational corporations (MNCs) to combat the current crisis. The present globalisation means increasing integration of national economies with the international markets, based on neoliberal economic policy and increased reliance on MNCs and market forces for resource mobilisation. Neoliberal globalisation has drastically reduced tariffs and liberalised trade in manufacturing, agricultural commodities and services. (Siddiqui, 2019d; also 2009).

Since India implemented a neoliberal policy in 1991, the state has gradually withdrawn its support to farmers. In the name of market efficiency, industries in the public sector have been privatised. And even critical services such as education and healthcare are being privatised, further increasing the burden on the poor, because the government would not like to be downgraded by the international credit agencies. Hence, it takes all the steps demanded by global capital so that the country may be seen as investment-friendly for foreign investors.

IV. Globalisation and Economic Crisis

With inefficiency and competition, neoliberalism has become the new orthodoxy. According to David Harvey (2005:3), “Neoliberalism has, in short, become hegemonic as a mode of discourse. It has pervasive effects on ways of thought to the point where it has become incorporated into the common-sense way many of us interpret, live in, and understand the world.”

Under the World Trade Organisation (WTO), capital liberalisation has made money flow more easily for foreign investors to take advantage of globalisation in the capital market. As a result, foreign capital investment has risen sharply. Still, it has remained unevenly distributed to a few regions, i.e., East Asia and China, but there is no diffusion of capitalism in many developing countries (Siddiqui, 2018c; also, 2018d). Moreover, despite the increase in foreign investment in India, for instance, there is no reduction in the levels of unemployment, and underemployment remained very high, even after more than three decades of neoliberal economic reforms in the country.

The globalisation of finance helps to reduce inflationary pressure in the advanced capitalist economies by imposing income deflation and squeezing purchasing power in developing countries. This is not done through raising direct taxes, as was the case during the colonial period, but now through cuts in government spending such as health and education, which ultimately increases the burden on the common people.

Global finance likes to keep fiscal deficits as a proportion of the GDP under strict control. This implies that fiscal deficit as a percentage of GDP cannot be increased. As Keynes suggested, it also means that aggregate demand cannot be expanded through state intervention. We also find that globalisation of finance and capital liberalisation undermines the economic sovereignty and autonomy of the state, because it imposes a limit on the fiscal deficit as a percentage of GDP.

State expenditure can only raise the aggregate demand if it is financed by taxing the capitalists or by fiscal deficit. But if the state taxes the workers and spends, that will reduce workers’ income and adversely affect demand levels. As is known, workersʼ marginal propensity to consume (MPC) is much higher than that of capitalists. Therefore, if the government spends by taxing the workers, there will be no net increase in demand levels.

The globalisation of production through shifting production locations to low-wage developing countries is the most significant development in the neoliberal period. Its main driving force is what some economists call “global labour arbitrage”, the efforts by MNCs largely based in advanced economies, such as North America, the European Union and Japan, to reduce costs and raise profits by replacing high-wage domestic labour with cheaper labour in the developing countries. And this is happening mainly by moving production (i.e., “outsourcing”) or through the immigration of workers. This is achieved via the WTO through the reduction of tariffs in the case of manufactured goods, and the removal of barriers to capital flows has rapidly increased the shifting of production to low-wage countries.

This is a new development because, during the colonial period, European companies only invested in mines and raw-material production, and manufacturing and technology were kept with the centre. There was a negligible transfer of technology to the peripheries. And the colonies always remained dependent on imports of manufactured goods from their colonisers. Therefore, neoliberal globalisation must be seen as a new stage of capitalist development, where imperialism is defined by economic essence, i.e., the exploitation of labour in the developing countries by the advanced capitalist countries.

A close examination of neoliberal globalisation reveals global labour arbitrage, arising from a higher degree of exploitation taking place in the low-wage countries, to be very important for the advanced capitalist countries in achieving higher rates of profits. Although Karl Marx excluded colonies from his main analysis, he did comment in Grundrisse (1973:651), “As long as capital is weak, it relies on the crutches of the past mode of production… As soon as it felt strong, it threw away the crutches and moved in accordance with its own laws. As soon as it begins to sense itself and become conscious of itself as a barrier to development, it seeks refuge informs that by restricting free competition, seem to make the rule of capital more perfect but are at the same time the heralds of its dissolution and the dissolution of the mode of production resting on it.” This is very similar to the argument that Lenin (1964:265) made three decades later, that “capitalism only became capitalist imperialism at a definite and very high stage of its development when certain of its fundamental characteristics began to change into their opposite when the features of the epoch of transition from capitalism to a higher social and economic system had taken shape and revealed themselves in all spheres.”

Historians characterised the first wave of globalisation in the eighteenth century simply as imperial relationships for economic exploitation and plunder. As a result, the disparities between countries have accelerated for the last two centuries following the Industrial Revolution in Europe with several waves of globalisation, which did little to reduce global inequalities. Rather, such a development strategy has increased inequalities between nations.

The latest wave of globalisation was in 1991 with the collapse of the Soviet Union. The relationship has not arguably changed much but has been replaced by a ‘centre-periphery’ relationship. This is often based on a centre that is well endowed with capital and technology and higher levels of productivity and skills, while the periphery is characterised by the mass availability of unemployed cheap labour, with overwhelming reliance on the primary commodity. The situation creates tensions, which often come out in the apportioning of blame for both underdevelopment and ensuing conflict.

Moreover, the recent wave of globalisation and the liberalisation of trade and capital has contributed to deindustrialisation in most developing countries and led to the undermining of national food security and foodgrain sovereignty. For example, the impact of the earthquake of 2010 in Haiti became severe due to the trade liberalisation policy undertaken earlier by the government under pressure from the IMF. The adoption of trade liberalisation resulted in many Haitian farmers abandoning rice cultivation and, with few employment opportunities available, migrating to town.

Early capitalism socialised the labour force between firms, but later, monopoly capitalism deepened the technical division of labour. After that, rather than vigorous competition in the recent period, capitalism increasingly manifested the decadent monopoly phase of rentiers, diverted resources from production, and undermined competition.

There were periodic bubbles in the advanced economies, such as the dot.com bubble in the 1990s in the US. These bubbles give a temporary impression that the economy is moving up. Since the 2008 global financial crisis, advanced capitalism has been under a protracted crisis.

The relocation of capital from the developed countries of the north to low-wage countries of the south (developing countries) in the current era of globalisation has received much attention. However, little attention was paid to the reallocation of labour. Workers from the comparatively lower-wage countries of Eastern Europe have migrated in large numbers to the developed countries. In fact, since the collapse of the Soviet Union and the adoption of the EU in the late 1990s, free mobility of labour has become a powerful inducement for these Eastern European countries to join the EU. Some of these countries have started displaying certain classic symptoms of labour-exporting economies: declining absolute populations, a shift in the composition of the population from able-bodied males of working age to children, mothers, and older people, and a change in the character of the economy from being productive to being remittance-receiving. The EU and IMF did not provide any comprehensive domestic job creation programme, and it was rather left to market forces to mobilise resources and create growth.

For example, workers from Latvia, Poland, Romania, and Bulgaria have migrated considerably to the developed countries of Western Europe and North America for the last two decades. In Bulgaria, the population declined by 11.5 per cent over the previous decade, from 7.3 million to 6.5 million. Similarly, in Romania, the population was 23.2 million in 1990 but declined by 16.4 percent to 19.4 million by 2021. Latvia had a population of 2.3 million in 2000, which had fallen by 18.2 per cent to 1.9 million by 2021. The decline in Estoniaʼs and Lithuania’s populations is similar in order of magnitude over a comparable period.

Of course, this is not the first time that capitalism has witnessed the relocation of capital and labour within the domain it controls. On the contrary, there has been such relocation in every phase of capitalism, except that the relocation patterns in the different phases have been different. Before the mid-nineteenth century, the relocation of labour was a racial and very cruel form of the transatlantic slave trade to the Americas and the Caribbean. From the mid-nineteenth century until the First World War, the relocation of capital took the form of European investment in the “New World”, which contributed to a massive diffusion of capitalism. This strategy was financed by the “drain of wealth”. The other was the migration of Indian and Chinese labour to the tropical and semi-tropical regions of the world (Siddiqui, 2018b).

With the development of capitalism in Britain as a merchant and banking capital from the latter part of the eighteenth century, the country invested heavily in colonial and overseas operations, including slavery, which was backed by the state and the navy. By the second half of the eighteenth century, industries began to develop and industrial capital emerged, detached from the City of London based on the nexus of merchants, bankers, and aristocrats. However, this has disadvantaged manufacturing ever since. The bankers and traders were unwilling to lend to manufacturers, and were always more interested in overseas.

In 1900, nearly 50 per cent of the total British capital was invested abroad. As Norfield notes: “In 2013, Britain had the second-largest stock of foreign direct investments [after the US] … Among the top 500 global corporations in 2011…the UK was in second place behind the US, with 34 companies…Of the world’s top 100 non-financial corporations in 2013, ranked by the value of their foreign assets, 23 were US companies, 16 were British, and 11 were French, while Germany and Japan each had ten” (cited in Calinicos, 2016). After the First World War, despite Britain’s imperial decline, it was still able to maintain the power of the City of London. And after the Second World War, the country created tax heavens for rich foreigners.

In contrast to Germany and Japan, there has been a close relationship between banks and industry. However, in Britain, industries have had to rely for their financial needs on the stock exchange and have had to pay high dividends to shareholders. From the late nineteenth century, rentiers and speculative capital were reinforced by the development of large urban property estates on high commercial rents, which were closely connected to the banks. Also, the exchange rate and monetary policy were geared to the interests of financial capital.

In the post-war period, there were strict capital controls, and the relocation of labour took the form of the migration of labour (in limited numbers) from ex-colonies or dependencies to the metropolis, such as from India, Pakistan and the West Indies to England, from Algeria and Morocco to France, and from Turkey to Germany. By contrast, the current period has seen a notable shift of capital from the metropolis to the former colonies and the migration of labour from Eastern Europe to the advanced capitalist countries. The chief motivation for both shifts from the point of view of capital has been the search for cheap labour.

Mainstream economists do not take the relocation of capital and labour into consideration. Their model analyses trade in goods and services in the absence of the relocation of capital and labour. A country with more capital per unit of labour cannot export capital to another country with less capital per unit of labour. Hence, it is supposed to do the “next-best thing”, which is to export capital-intensive products to them, and import labour-intensive products in exchange.

With the decline of the US economy and growing competition with China, the US has experienced a long-term decline in its share of global GDP. In the meantime, China has emerged as a leading manufacturing and exporting country, posing a challenge to US hegemony, which suffered a huge blow during the 2008 global financial crisis.

Despite the closure of certain industries due to globalisation, the US has profited hugely from the globalisation of production and the free flow of goods and capital. Moreover, the five global IT MNCs known as “FAANGs” (Facebook, Amazon, Apple, Netflix, and Google) represent the US ambition of dominating the world. These giant companies are a major stake in US conflicts with China.

Nevertheless, Professor Robert Brenner (2020) notes that the March 2020 government bailout of markets shows that “With the US economy performing so badly… the bipartisan political establishment and its leading policymakers have come to a stark conclusion that the only way that can assure the reproduction of the non-financial and financial corporations, their top managers, and stakeholders – and indeed the top leaders of the major parties who are closely connected with them – is to intervene politically in the asset markets and throughout the whole economy, to underwrite the upward redistribution of wealth to them by direct political means… For a long epoch, what we have had is worsening economic decline met by intensifying political predation.”

Economic crises under capitalism are primarily crises of accumulation, that is, saving and investment dynamics. Investment in new productive capacity or existing companies is what determines economic growth. Such investment decisions are governed by expected profits on new investments. The decline in the long-term growth rate experienced by the advanced economies of the US, the UK, France, and Japan over the last four decades can be seen as mainly related to shrinking net investment. The existing excess capacity in businesses is due to the fact that their monopolistic nature tends to reduce the expected profits on assets. The US economy has also witnessed a long-term decline in power utilisation in manufacturing, which averaged 78 per cent from 1971 to 2021, well below levels that stimulate net investment. This means that the capital accumulation process within production has stagnated.

In contrast to the shrinking net investment in the advanced economies, China has a “high growth ratio” standing for investment as a share of economic surplus. Economic surplus is the difference between national output and wage income. China has invested nearly 80 per cent of its economic surplus, which resulted in high growth rates of almost 8 per cent annually between 1980 and 2010. In contrast to the Chinese growth experiences, the advanced capitalist economies had a relatively low growth rate, investing less than 45 per cent of the economic surplus, which resulted in more than four decades of lower average economic growth rates.

Corporate investments are not dependent on the prior availability of savings. As Schumpeter said, capitalism is a system that creates “credit ad hoc”, and Keynes emphasised that investment determines savings, not vice versa. It is important to note that the cash funds of corporations in the phase of monopoly-finance capital far exceed profitable investment opportunities. For example, by December 2020, non-financial corporations had cash funds of more than US$5 trillion. Much of this was parked abroad in tax havens, and such amounts have tripled since 1991.

V. Inequality Crisis

Thomas Piketty has documented that income inequality has risen under neoliberal globalisation everywhere. The important study by Piketty (2014) indicates that inequality has been growing unabated in all capitalist economies since the adoption of neoliberal economic reforms in the 1980s. His central argument is that inequality is not an accident but a necessary feature of capitalism, and certainly, state intervention only could reverse it. In India, for instance, after adopting neoliberal reforms in 1991, despite increasing GDP growth rates up to 6 per cent per annum from 1991 to 2010, most people’s income has not risen. Still, the top 1 per centʼs share in the national income has gone up from 6 per cent to nearly 16 per cent during the same period. Government data for 2019 reveals that the richest 1 per cent of Indians own almost 60 per cent of the country’s wealth while the richest 10 per cent own as much as 81.5 per cent of the wealth. Marx termed it “the absolute general law of capitalist accumulation, huge accumulation at one pole, while rising misery at the other pole”.

The growth of inequality in the US of the last fifty years is presented in detail in a study by the Organisation for Economic Co-operation and Development (OECD). The study estimates the effect of major tax cuts given to the rich over this period. Significant reforms reducing taxes on the rich, as might be expected, lead to greater income inequality, as measured by the share of pre-tax national income going to the top 1 per cent. “The size of the effect is substantial” and “the effect holds in both the short and medium-term.” Research has found that there is no benefit to the economic performance of such regressive tax cuts. The trajectories of real GDP per capita and the unemployment rates for OECD nations were unaffected by significant reductions in taxes on the rich in both the short and medium term (OECD, 2022).

Mainstream economists argue that low interest rates stimulate private investment because they lower the cost of borrowing. But low interest rates could also stimulate asset price bubbles. When the “dot.com bubble” in the US collapsed two decades ago, Federal Reserve chairman Alan Greenspan lowered interest rates, which stimulated a new bubble, the housing bubble, in the US. This artificially boosted the wealth of some individuals by increasing their consumption expenditure, and increased investment in the housing sector.

The US government purchased the debt of Fannie Mae and Freddie Mac, and in 2008 the Fed extended an US$85 billion credit to the American International Group (AIG). Such a policy by the Fed has brought an enormous expansion of the number of assets on its balance sheet. The Emergency Economic Stabilization Act of 2008 passed by the US Congress provided up to US$700 billion for the relief to purchase distressed assets and for capital injection into financial institutions.

In 2009, the Obama administration adopted a different economic policy in contrast to the 1930 Great Depression to deal with the 2008 global financial and economic crisis. If this effective policy and government intervention had not been adopted, as was the case during the 1930 Great Depression, the economic recession and downturn of the fall 2008 crisis would have turned out to be another Great Depression, and the fallout of 2008would have been much greater.

During the Great Depression of the 1930s, the Hoover administration tried to establish a balanced budget, because it was thought to bring economic recovery. A balanced budget was also sought so that it could help to stabilise the US dollar under the gold standard, because it was thought at the time that fiscal policy intervention would obstruct economic recovery. The Smoot-Hawley Tariff Act of 1930 was passed, which raised tariffs very high during the Great Depression to protect domestic industries in the US.

In India, even though a high growth rate has been observed during the neoliberal policy period, job opportunities have been negligible. Those segments of the population who are beneficiaries of neoliberal globalisation are integrated with the international financial capital and upper-middle-class professionals. Still, farmers, small producers, and the lower-middle classes have been adversely affected.

Keynes (1930) suggested that capitalism was a flawed system which resulted in high levels of unemployment. Therefore, the state is needed in order to rescue capitalism. However, at present, the globalisation of finance does not allow it. Globalised finance has undermined the role of the nation-state to remove demand bottlenecks. After COVID-19, the US government adopted a policy that was an exception, as also happened after the 2008 economic crisis. This was possible because the US dollar is considered “as good as gold”, meaning that the US government intervention did not trigger any large-scale exodus of finance.

However, the governments of the developing countries were not able to stimulate their economies adequately, because their fiscal policies were constrained by the conditions imposed upon them by the IMF to restrict their fiscal deficits relative to GDP. On the other hand, their monetary policies had to be tied to the monetary policy of the US. Their interest rates, for instance, had to be sufficiently higher than the US interest rate; otherwise, there would be serious financial outflows.

VI. Conclusion

In a capitalist mode of production, credit accelerates the growth process, and sellers expand their markets by selling their commodities on credit. Buyers extend their business beyond their actual capital by buying commodities on credit. Lehman Brothers went bankrupt in 2008, and the US economy plunged into a deep crisis, beginning the 2008 global financial crisis. At the G20 summit meeting in 2009, it was recognised that other emerging economies like China, India, Brazil, and Russia could contribute by keeping their economies open to international cooperation. Thus, the adverse impact of the recession would be minimal.

In the past, particularly in the case of developing countries, the IMF had always pressured them to “open up” their economies to the penetration of Western capital, with the policy change including lowering taxes on businesses and adopting anti-worker and austerity measures. In the name of “pro-market policy”, the IMF and World Bank advised the developing countries to sell their natural assets, such as land and mines, to MNCs to increase inflows of capital and efficiency.

Study has found that capitalism always needs new territories (markets) for its growth and its drive to accumulate more, and to achieve this, it needs direct or indirect control of other countries. This is why capitalism has launched wars to control other countries and economies since its birth and, even now, insurgency and instability in developing countries are closely linked to outside interference. Capitalism has created huge inequality between nations, unprecedented in human history.

Both colonialism and imperialism were forms of conquest that benefited European powers economically and politically. Imperialism was the necessary and inevitable result of the logic of accumulation. And US imperialism means American economic and political hegemony, regardless of whether it is exercised directly or indirectly. Although Karl Marx never developed a theory of colonialism, his analysis of capitalism focused on capitalismʼs inherent tendency to expand in search of new markets. Expansion is a necessary product of the core dynamic of capitalism: overproduction. Competition among producers drives them to cut wages, which leads to a crisis of under-consumption.

David Ricardo’s “comparative advantage” international trade theory made colonialism morally defensible. The theory maintains that those countries can benefit from trade even if they do not have an absolute advantage in producing any goods, so long as they specialise in goods with relatively higher productivity. If countries pursue this comparative advantage, then trade generates win-win outcomes whereby all nations involved in trade are able to maximise income, and the consumers have access to cheaper commodities. Mainstream economists support the theory and claim that it promises mutual gains through global integration. Ricardo’s classical example (where Britain produced wine and cloth less efficiently than Portugal) painted Britain as the weaker economic power. But, Britain had just “liberated” Portugal from Napoleon (in 1808), subordinating it to its own “imperialism of free trade”. In contrast to David Ricardo’s trade model, Karl Marx emphasised the historically unique social relations of capitalism as arising out of the co-constitutive processes of mercantile colonialism and “primitive accumulation”. Consequently, “capital comes [into the world] dripping from head to foot, with blood and dirt from every pore.”

Mainstream economists support David Ricardo’s comparative advantage trade theory, which assumes that free trade benefits all trading partners, even though the long colonial experience clearly showed the destructive, deindustrialising consequences of “free trade”. There are no such past examples to prove otherwise. Indeed, trade liberalisation in agriculture, as supported by these international institutions’ attempts to undermine foodgrain security (Siddiqui, 2021e), would mainly benefit advanced capitalist countries that happened to be large foodgrain exporters in the world markets. The destruction of foodgrain self-sufficiency, as has happened in several African countries, will make the developing countries vulnerable to famines and balance of payments crises.

In short, the regime of neoliberal globalisation has run into a dead end. Since the collapse of the Soviet Union and the emergence of the US as the sole global power, globalisation has been imposed on the developing countries through the IMF, the World Bank, and the WTO. It amounts to the integration of economies into a single global market under the increased control of MNCs over world resources and markets. But it has also led to global overproduction, and to its countering through increased financialisation and credit expansion, leading to the formation of asset price bubbles. Pursuing such policy measures ended in the 2008 global financial crisis and plunged the world’s economy into economic turmoil.

It seems that the present neoliberal globalisation is meant to control the assets of developing countries. For example, in India, during the anti-colonial struggle by the Congress Party leaders, natural resources would remain with the state, being owned, and developed by it. However, under the neoliberal policy, foreign capital is invited once again to develop natural resources in the country.

Economic sovereignty is crucial for any long-term economic development in the former colonies. The term “economic sovereignty” means the power of national governments to make decisions independently. Today, national sovereignty continues to be under pressure via international financial institutions to adopt neoliberal globalisation. The escalation of imperialist aggression is very visible in the former colonies. We may call it neocolonialism and, as Samir Amin (2003) observed, at present capitalism has become an obsolescent system.

The demise of Bandung and the Soviet Union and the permanent crisis of monopoly capitalism have brought the world into a deeper political-economic crisis. Under current neocolonialism, monopoly-finance capitalism has escalated the drain from the peripheries, and also declining compensation to the working classes in advanced capitalist countries. The US has continued to escalate its interventions and create instability in the peripheries. Up to the present, neocolonialism has been marked by the decline of nationalism and the rise of comprador elites in the peripheries.

About the Author

Dr Kalim Siddiqui is an economist, specialising in International Political Economy, Development Economics, International Trade, and International Economics. His work, which combines elements of international political economy and development economics, economic policy, economic history and international trade, often challenges prevailing orthodoxy about which policies promote overall development in less developed countries. Kalim teaches international economics at the Department of Accounting, Finance and Economics, University of Huddersfield, U.K.. He has taught economics since 1989 at various universities in Norway and U.K.

Dr Kalim Siddiqui is an economist, specialising in International Political Economy, Development Economics, International Trade, and International Economics. His work, which combines elements of international political economy and development economics, economic policy, economic history and international trade, often challenges prevailing orthodoxy about which policies promote overall development in less developed countries. Kalim teaches international economics at the Department of Accounting, Finance and Economics, University of Huddersfield, U.K.. He has taught economics since 1989 at various universities in Norway and U.K.

References:

• Armstrong, P. and K. Siddiqui. (2019). “The case for the ontology of money as credit: money as bearer or basis of value”, Real-World Economics Review, no.90:98-119.

• Brenner, R. (2020). “Escalating Plunder”, New Left Review, no.123, May-June, London.

• Harvey, D. (2005). A Brief History of Neoliberalism, Oxford: Oxford University Press.

• Johnson, Chalmers. (1995). Japan: Who Governs?, New York: W.W. Norton & Co.

• Keynes, J.M. (1930). The Great Slump of 1930, London: The Nation & Athenaeum.

• Lenin, V.I. (1964). “Imperialism, the Highest Stage of Capitalism” in Collected Works, vol.22, Moscow: Progress Publishers.

• Marx, Karl. (1973). Grundrisse, London: Penguin Books.

• Piketty, Thomas. (2014). Capital in the 21st Century, Cambridge, MA: Harvard University Press.

• Saad-Filho, Alfredo. (2010). Growth, Poverty and Inequality: From Washington Consensus to Inclusive Growth. DESA Working Paper ST/ESA/2010/DWP/100.

• Schumpeter, Joseph. (1976). Capitalism, Socialism and Democracy, London: George Allen and Unwin Ltd.

• Sen, Amartya K. (1981). Poverty and Famines: An Essay on Entitlement and Deprivation, Oxford: Oxford University Press.

• Siddiqui, K. (2021a). “The Import Substitution Policy in the Post-Colonial Countries”, World Financial Review, Nov-Dec., 76-84.

• Siddiqui, K. (2021b). “The Political Economy of Industrial Policy”, World Financial Review, May-June, 58-66.

• Siddiqui, K. (2021c). “Trade Liberalisation, Comparative Advantage, & Economic Development: A Historical Perspective”, World Financial Review, May-June, 65-73.

• Siddiqui, K. (2021d). “The Importance of Industrialisation in Developing Countries”, World Financial Review, Jan-Feb. 60-73.

• Siddiqui, K. (2021e). “Agriculture, Sustainable Development, and the Government Policy in the Developing Countries”, World Financial Review, January-February. 44-59.

• Siddiqui, K. (2021f). “The Study of International Political Economy”, World Financial Review, July-August, 46-56.

• Siddiqui, K. (2020a). “Britain’s Trade with China in the Eighteenth and Nineteenth Century: A Review of the Opium Wars”, Asian Profile, 48(3): 207-21, Sept.

• Siddiqui, K. (2020b). “The Political Economy of Famines under Colonial India: A Critical Analysis”, World Financial Review, July-August, 56-70.

20. Siddiqui, K. (2020c). “Can Global Imbalances Continue? The State of the United States Economy”, Argumenta Oeconomica Cracoviensia, 23(2):11-32.

• Siddiqui, K. (2020d). “The US Dollar and the World Economy: A critical review”, Athens Journal of Economics and Business, 6(1):21-44.

• Siddiqui, K. (2020e). `The Study of Economic History and the Importance of Understanding the Past”, World Financial Review, Nov.-Dec,, 46-59.

• Siddiqui, K. (2019a). “The Political Economy of Global Inequality: An Economic Historical Perspective”, Argumenta Oeconomica Cracoviensia, 21(2):11-42.

• Siddiqui, K. (2019b). “Financialisation, Neoliberalism and Economic Crises in the Advanced Economies”, World Financial Review, May-Jun., 22-30

• Siddiqui, K. (2019c). “The Political Economy of Essence of Money & Recent Development”, International Critical Thought, 9(1):85-108.Taylor & Francis.

• Siddiqui, K. (2018a). “The Political Economy of India’s Economic Changes since the last Century”, Argumenta Oeconomica Cracoviensia, 19:103-32.

• Siddiqui, K. (2018b). “Capitalism, Globalisation and Inequality”, World Financial Review, Nov.-Dec., 72-7.

• Siddiqui, K. (2018c). “David Ricardo’s Comparative Advantage and Developing Countries: Myth and Reality”, International Critical Thought, 8(3):1-28, Taylor & Francis.

• Siddiqui, K. (2018d). “U.S. – China Trade War: The Reasons Behind and its Impact on the Global Economy”, World Financial Review, Nov.-Dec., 62-8.

• Siddiqui, K. (2018e). “The Political Economy of India’s Post-Planning Economic Reform: A Critical Review”, World Review of Political Economy,9(2):235-64.

• Siddiqui, K. (2018f). “Imperialism and Global Inequality: A Critical Analysis”, Journal of Economics and Political Economy, 5(2):266-91.

• Siddiqui, K. (2016). “International Trade, WTO and Economic Development”, World Review of Political Economy, 7(4):424-50.

• Siddiqui, K. (2015a). “Political Economy of Japan’s Decades-Long Economic Stagnation”, Equilibrium Quarterly Journal of Economics and Economic Policy, 10(4):9-39.

• Siddiqui, K. (2015b). “Economic Policy: State versus Market Controversy”, (ed.) A.P. Balcerzak. Contemporary Issues in Economy: Market or Government, 39-63, European Regional Science Association, Poland.

• Siddiqui, K. (2015c). “Trade Liberalisation and Economic Development: A Critical Review”, International Journal of Political Economy, 44(3):228-47.Taylor & Francis.

• Siddiqui, K. (2013). “A Review of Pakistan’s Political Economy”, Asian Profile, 41 (1):49-67.

• Siddiqui, K. (2009). “The Political Economy of Growth in China and India”, Journal of Asian Public Policy, 1(2):17-35, March. Routledge.

• Siddiqui, K. (1990a). “Historical Roots of Mass Poverty in India” (ed.) C.A. Thayer, J. Camilleri, and K. Siddiqui. Trends and Strains. 59-76, New Delhi: Peoples Publishing House.

• Siddiqui, K. (1990b). “Political Economy of Terrorism” (ed.) V.D. Chopra. Genesis of Indo-Pakistan Conflict on Kashmir,212-25, New Delhi: Patriot Publishers. ISBN 81-7050-124-5.

• Steward, Frances. (1995). Adjustment and Poverty Options and Choices, London: Routledge.

Population Could Create a Devastating Global Slowdown")

{kind=link}