All business is centered on solving customer problems. The problems can range from where to eat to putting satellites into orbit. And the solutions can be as simple as a dinner menu to as complex as a SpaceX Super Heavy rocket. But merely identifying customer problems and solutions is insufficient to start a business. Your proposed solutions must be wrapped around a business model.

Not all businesses are created equal. Some businesses are simply better than others. The differences sometimes touch on the size of the problems to be solved and the market potential for problem-solving products and services. But mostly, the qualitative differences come down to business model fundamentals.

Step 1: Business Models Start with Revenues

Developing a business model starts with revenue expectations. What to charge depends on the value of the service to be provided together with customer alternatives. Some companies seek to encourage demand by keeping prices low, while others believe it to be better to sacrifice demand for premium pricing. Some companies seek to bundle services or products into a single price point, while others seek to charge for each service or product in what might be described as an a la carte strategy. Then again, some companies, such as Google, do not charge their customers at all, instead charging others for customer and data access. In a real way, such companies have two sets of customers, with one set paying for a solution and another set getting their solutions for free.

Once you have a fee schedule, you can start to estimate the annual fees to be realized. From there, it becomes important to estimate your expected revenue growth rate. There are three sources of revenue growth. The best of these entails getting more customers each year. The second revenue growth source is centered on your ability to increase prices. The final source of revenue growth is the development of new offices or locations. This last form of growth is common for many businesses that need new locations to grow their accessible market (think restaurants, fitness clubs, retailers and similar businesses).

Step 2: Operating Costs

Now that you have an idea of expected annual revenue streams, you are ready to turn to the next step of business model design: Considering the costs you will have to incur to operate your business. This includes the following:

- The cost of materials used to manufacture or buy the products you propose to sell.

- The people you will need to hire to design, create and deliver the products or services you propose to sell, including yourself and other management team members.

- Supporting personnel needed to manage your office and produce your financial reporting.

- The cost of outside services, including legal, accounting, cleaning service providers and others.

- Corporate insurance, employee health insurance and other employee benefits and costs.

- Telephone, network, travel costs and software and other subscriptions needed to operate your business.

- Rental expense on your office space and anything else where buying the real estate or related equipment is not an option.

Note that I have omitted non-cash accounting conventions, such as depreciation.

You probably have material capital equipment requirements, from real estate to manufacturing equipment to transportation equipment. Often, you will have a choice to either rent or own such assets. For now, to make this simple, we will leave these potentially large costs out of your expense budget. We will simply initially assume that you pay cash for these items and own them. We are making a business model without the use of borrowings or lease proceeds.

When considering your operating costs, a key consideration is whether you prefer to manage every aspect of your business or whether they may be tasks that are worthwhile outsourcing. For instance, your company may manufacture a product, in which case they may be an option to retain design oversight while outsourcing product manufacture. You may be able to outsource some of your financial reporting, IT needs and other back-office requirements. Often, outsourcing can reduce operating costs. Outsourcing can also lower your business space requirements. At the very least, outsourcing can simplify your business model while reducing risk by converting potentially large fixed operating costs into more bite-sized variable costs.

Now that you have your estimated sales and operating costs, you can estimate your operating profit margin, which is simply the difference between revenues and costs shows as a percentage of revenues.

Step 3: Business Investment

There is one major business model task in front of you. It’s time to determine your required business investment, or the amount of corporate assets you will need. Here are the five major components of business investment:

- Real estate and equipment

- Prepaid costs

- Inventory

- Accounts receivable

- Cash

The five major corporate asset variables do not alone define business investment. Missing from this calculation is the money your company gets that is free. When thinking of free money, the first thing that comes to my mind is supplier trade payables, where you receive title to inventory without having yet paid for it. Since trade payables are interest free, they serve to lower the amount of money your company needs to invest in inventory. If your business is a restaurant, supplier payables might actually be ten times larger than inventory, meaning that you have no inventory cash needs and that supplier contributions help pay for other business investment requirements. In restaurants, it is common for inventory to turn over every three days, while suppliers might offer generous thirty-day payment terms.

The second commonplace free money is generally less impactful. It is in the form of accruals, where you incur costs, such as wages and other expenses, but do not pay for them right away.

One of my favorite sources of free money that bears mention is customer deposits, where you ask your customers to prepay for part or all a product or service. Money received up front from customers can be impactful. Anytime you purchase a gift card, you are making a customer deposit, helping a business lower its business investment requirement by giving it free money.

Business investment is the five major asset components, less any free money. Business Investment is the net amount of the five assets that need to be funded with borrowings and lease proceeds or shareholder equity. Business investment is what is funded by money seeking a return.

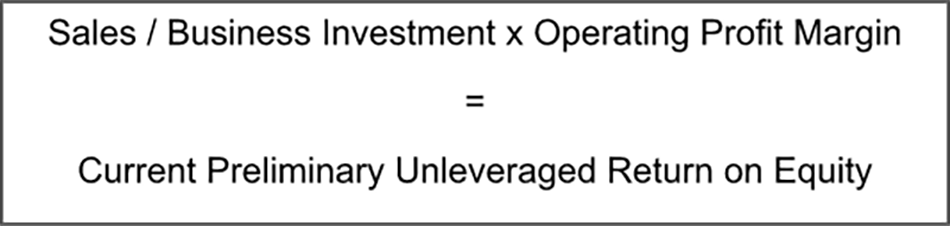

Step 4: Computing Your Preliminary ROE

Investor returns arising from business model creation start with knowing your expected current rate of return on equity. To do this, you simply start with three numbers: Sales, Business Investment and Operating Profit Margin. Assuming you are funding business investment completely with equity, a preliminary unlevered rate of return would look like this:

The first part of the three-variable equation (Sales / Business Investment) can also be written as a ratio (Sales:Business Investment). I find using a ratio preferable to focusing on absolute sales and business investment numbers. Once you start to focus on relationships, numbers cease to matter and your business model can come into focus. Starting your model without using leverage increases the simplicity. The best businesses models have the highest rates of unlevered return.

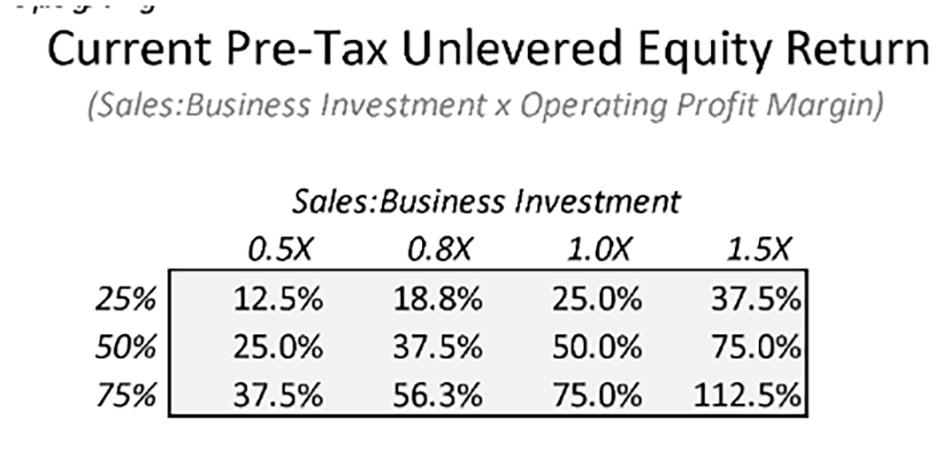

Now, arriving at an estimate of your model’s total rate of pre-tax equity return becomes simple. The first step is to create a universal matrix of current pre-tax equity returns using different operating margin and sales:business investment ratios.

Note the similarity of the relationships. If your business model has a sales:business investment ratio of .5X and an operating profit margin of 75%, your current pre-tax equity return is 37.5% annually. If you triple your sales:business investment ratio to 1.5X, while your profit margin falls to a third of its prior value, your current pre-tax equity rate of return is the same. When it comes to current equity rates of return, the importance of operating profit margins and sales:business investment ratios is the same.

The equivalence of operating margins and sales:business investment ratios means that it is important for business model creators to spend equal amounts of time optimizing each. If you can outsource production such that your sales:business investment ratio rises by more than your profit margin, your business model and current equity rates of return will be better. If you can do more with less (both expenses and business investment), your business model will improve. The corporate benefits of business investment reductions are behind the importance of supply chain management, including just in time inventory. The same goes for corporate efforts to shorten customer payment terms or receive customer deposits, both of which likewise serve to reduce business investment.

The goal of any business model is to first optimize your unleveraged current pre-tax equity rate of return. The effort that goes into this endeavor can be highly creative as you look to your three key relationships between your sales, business investment and operating profit margin.

Step 5: Computing Your Current Pre-Tax ROE

The current unleveraged pre-tax rate of return from your estimates of sales, business investment and operating profit margin get you most of the way through your business model design. There is just one component missing to get you to your current unlevered pre-tax equity return: The annual amount of maintenance capital expenditures you need to replace worn out equipment or periodically remodel your facility.

When it comes to thinking about annual maintenance capital expense requirements, I tend to use long-run averages, because some years will have heavier capital cost needs than others to maintain your business. Once you know the average amount of money you expect to spend annually, all you need to do is to create another ratio:

Showing this ratio as a percentage, simply subtract it from the current unlevered ROE computed with sale, business investment and operating profit margin. The result is your final estimated current unlevered pre-tax rate of return. I find that most companies tend to spend between 2% and 4% of their business investment annually to maintain it. In this case, if your sales:business investment ratio is 1:1 and your operating profit margin is 50%, your current unleveraged pre-tax rate of return per the first table would be 50%, less 2% to 4%.

You might be thinking that the small relative size of the maintenance capital expenditures means that they require less business model thought. Per the preceding example, the preliminary current pre-tax unlevered return is 50%, with maintenance capital expenditures lowering the return to 46%-48%. Of course, any savings in the amount of annual maintenance capital expense costs should not be sneezed at. But the capital expenditure bucket can have a far greater return impact.

Let’s say that you are a multi-unit retailer and that you periodically close underperforming locations. Or let’s say your company is acquisitive, buying a constant stream of operating businesses, but not all the acquisitions work out. If you suffer losses from the sale of shuttered properties or businesses, where would these losses appear in a business model? You got it. You’d include those annual losses as a percentage of business investment with your maintenance capital expenses. The result could be a far greater return on equity deduction.

Business leaders tend to spend the most time focusing on sales, business investment and operating profit margins. But capital expenses, especially if they include periodic investment losses, can loom large. As Warren Buffett has often said, “The first rule of business is to never lose money and the second rule of business is to never forget the first rule.”

Now, Can You Make $1 Million?

Your current pre-tax rate of return is the foundation of business value. Let’s say you have a sales:investment ratio of 1X, an operating profit margin of 50% and maintenance CapEx of 2% annually. Your current unlevered annual pre-tax rate of return is 48%. And lets’ say that you shop your business around and find that investors are willing to have a current pre-tax rate of return for a company having similar risk and growth prospects of 12% annually. In such a case, your company would be worth 4X what it cost you to assemble (48%/12%). In business terms, your valuation multiplier is 4.

Business value multipliers vary based on business model quality. In the case of Apple, Inc., which is the world’s more highly valued company having among the finest business models ever devised, the multiple is around 10X. While many companies have larger multipliers, they will be far smaller. It is important to keep in mind how incredibly large the equity investment is in Apple. Its equity investment began with the small contributions from founders and early investors but grew with its initial public offering and then with the reinvestment of billions of dollars in cash flows over forty years.

Can your business idea be worth $1 million? Just take the equity to be invested at cost and multiply it by four.

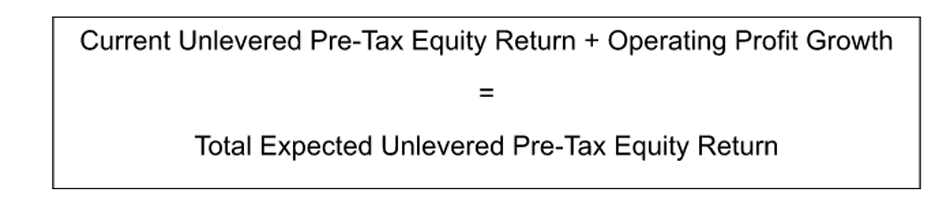

When it comes to business valuation multipliers, your growth in operating profits that is expected to arise from sales growth and reinvested cash flows is important. The greater the expected growth, the greater the business valuation multiplier. Growth is the bridge from your current pre-tax rate of return to your total expected pre-tax rate of return.

Our business model creation and valuation exercise has been basic. We have assumed no borrowings or lease proceeds and a company fully funded with equity. Of course, most founding investors need to use some degree of leverage to make their investments feasible. In fact, most founding shareholders will fall short of the equity funding needed to start a business at all. But that is a topic for later. For now, what you need to know is that a solid unlevered business model is an essential stepping off point to business creation. Having personally started some businesses, an important finding has been this: Solid business models and capable management teams are scarcer than the money needed to fund them.

If you have devised a customer solution, have gone through the five steps to determine business model viability and have a team to work with you to execute your plan, my advice is simple: Go for it.

About the Author

Christopher Volk, author of The Value Equation: A Business Guide To Creating Wealth For Entrepreneurs, Investors And Leaders, has been instrumental in leading and publicly listing three successful companies, two of which he co-founded. The most recent is STORE Capital (NYSE: “STOR”) where he served as founding chief executive officer and then as executive chairman. Volk, who has written about corporate finance since early in his career and has created an award-winning video series about the topic, is a regional winner of EYs’ Entrepreneur of the Year award. He is on the Board of Banner Health and is Chairman of the Board of Tenet Equity. Volk resides in Paradise Valley, Arizona, and Huntsville, Alabama. You can learn more at http://www.thevalueequation.com/

Christopher Volk, author of The Value Equation: A Business Guide To Creating Wealth For Entrepreneurs, Investors And Leaders, has been instrumental in leading and publicly listing three successful companies, two of which he co-founded. The most recent is STORE Capital (NYSE: “STOR”) where he served as founding chief executive officer and then as executive chairman. Volk, who has written about corporate finance since early in his career and has created an award-winning video series about the topic, is a regional winner of EYs’ Entrepreneur of the Year award. He is on the Board of Banner Health and is Chairman of the Board of Tenet Equity. Volk resides in Paradise Valley, Arizona, and Huntsville, Alabama. You can learn more at http://www.thevalueequation.com/

Population Could Create a Devastating Global Slowdown")

{kind=link}