By Wei Hongxu

In the quarterly meeting of its monetary policy committee, the People’s Bank of China (PBoC) repeatedly mentioned price stabilization in its policy statement. The trend of inflation in China is not only becoming a restrictive factor for monetary policy to support stable growth, but has also increasing impacted its economic recovery. This has also aroused worry in the market that with changes in the international situation, inflation will exceed the central bank’s 3% policy target, which could trigger passive adjustments in the policy or even hyperinflation in extreme cases.

Despite the spike in global inflation levels, inflation in China has remained relatively stable in recent years without significant fluctuations. Yet, as the international situation changes, what will happen to inflation in China? Will there be a situation of high inflation as in developed countries? As this is not only related to the process of economic recovery in the second half of the year, but also to the direction of future macro policy adjustments, it has been an issue of concern for the country’s policymakers.

When it comes to the issue of global inflation, researchers at ANBOUND have noted that high inflation in developed countries such as the United States and Europe may cause short-term outbreaks of aggregate demand under the post-pandemic monetary stimulus. In addition, there is also an imbalance in energy sources brought about by rising geopolitical risks. Factors like the restructuring of supply and demand during the pandemic and carbon reduction development policies have also brought long-term effects. Such circumstances would mean that economies with high dependence on energy and with heavy service industries have to face the threat of high inflation. Inflation in the United States was 8.6% in May, while the United Kingdom saw a record high of 9%, and the latest data showed that the inflation level in the eurozone reached 8.6% in June. There is the risk that the inflation problem is getting out of control, which forces major central banks in Europe and the United States to adopt tightening policies like raising interest rates and shrinking balance sheets to deal with the risks brought by inflation at the expense of economic slowdown or recession.

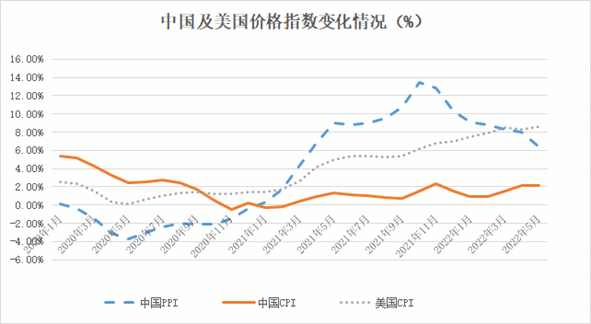

Price Changes in China and in the United States

Although China’s inflation did increase in the second quarter, the moderate rise in inflation did not form a fundamental constraint on the country’s economic development and monetary policy. This is mainly because its economic cycle is different from that of Europe and the United States. While China is also affected by external factors, the lack of domestic demand in the economy is still the main reason for changes in inflation. At the same time, the COVID-19 outbreaks in developed areas of the country in the first quarter of this year have had a great impact on China’s production and life, while the recovery of consumer and service demands has not seen a retaliatory rebound. Therefore, the recovery of demand as a whole requires a certain process. In the case of insufficient effective demand, it would be difficult for domestic inflation to change rapidly.

When it comes to the aspect of supply, it should be pointed out that China’s policies have placed a lot of emphasis on energy security and bulk commodities. This has essentially guaranteed the supply of resources, thus avoiding the occurrence of hyperinflation caused by externally imported inflation. As far as the domestic industry is concerned, China itself has a relatively complete industrial chain and supply system, which has also minimized the disturbance to production and supply caused by uncertain factors brought about by the adjustment of the global supply and industrial chains. On the one hand, through the monopoly of state-owned enterprises in industrial upstream, China has basically maintained the crude oil import channel even under the circumstance of crude oil price fluctuations. On the other hand, the coal-electricity linkage is used to maintain the stability of the electricity price of enterprises as much as possible. Although a large number of power generation enterprises have suffered losses, and there has also been the issue of “power cuts” in some places, the overall electricity price is still in a stable state. This greatly alleviates the impact of energy price fluctuations on business production.

Due to fluctuations in international energy and commodity prices, the increase in production prices as a “global factor” has continued for quite some time for China. The country’s PPI level will remain high for a long time from 2021. However, the widening of the scissors gap between PPI and CPI has not resulted in a short-term sharp increase in final consumer prices. Thanks to the continuous improvement of the production efficiency of enterprises, some of the pressure of rising costs has been absorbed. Meanwhile, in most traditional fields, under the situation of overcapacity, flexible production buffers the pressure of rising upstream prices, accelerates industrial integration, and passively achieves “de-capacity”.

In the iron and steel industry, where the problem of overcapacity is more prominent, since the outbreak of the pandemic, the price of crude steel products has not fluctuated much. At the same time, some leading enterprises are also accelerating the integration, which has alleviated the impact of fluctuations in energy prices and iron ore prices on the industry. This, in turn, has also eased the cost pressure on downstream enterprises. All these factors signify that the commodity price is continuously digested through the industrial chain, and finally, the terminal price is protected from the upstream influence.

In addition, the PBoC has always emphasized a “prudent” monetary policy, adhered to the policy of matching the growth rate of money and social financing scale with nominal GDP, and not over-issuing money. This in effect keeps the domestic money supply stable, which is the main factor for the basic stability of the RMB exchange rate and the stable domestic short-term price level. There is a clear difference between the environment within China and the international environment, which contributes to the overall stability after the COVID-19 outbreaks ended.

As the PBoC put forward the overall consideration of “stabilizing prices” and “stabilizing employment”, its focus should be on avoiding hyperinflation caused by food, energy, and supply chain constraints. This is especially true when it comes to “imported inflation” brought about by the uncertainties such as increased geopolitical risks and international capital flows. It is worth noting that the price of pork, which is the main component of the CPI, has undergone some changes in the context of the shifts in the pig cycle and the increase in food import prices, which may impact food prices and inflation trends. However, this change is more of a cyclical factor. According to the current situation of production and demand in China, when the industrial chain is complete and the logistics system is stable, it is unlikely that there will be an overall imbalance of supply and demand. This means that domestic inflation may rise moderately as the economy recovers, but there will be no hyperinflation.

Under the current situation, researchers at ANBOUND believe that among the triple pressures of demand contraction, supply shock, and weakening expectations, the main contradiction facing the Chinese economy is still demand contraction. Macro policy adjustments, including monetary policy, still need to focus on “stabilizing growth”. Only by stabilizing aggregate demand can employment issues and structural problems be solved. As far as monetary policy is concerned, it is still necessary for China to maintain a “moderately loose” tone to provide an appropriate monetary environment for economic recovery and stability. Of course, the issue of inflation cannot be completely ignored, but the coordination of other industrial policies and market supervision policies is needed to stabilize the supply chain, sustain a complete domestic production system, and maintain a balance between supply and demand, so as to effectively promote market recovery and sustainable growth.

Final analysis conclusion:

Inflation is not only a problem that major economies have to face, but also a potential risk factor in China’s economic recovery. For now, insufficient domestic effective demand is still the main factor restraining inflation. In the short term, China’s complete industrial chain, stable supply system, as well as its restrained monetary policy will play an important role in alleviating inflation. However, in the medium and long term, with the intensification of the international energy crisis and the surge in global inflationary pressure, the country still needs to be alert to the risk of high inflation.

About the Author

Wei Hongxu is a researcher with ANBOUND, PhD in economics from the University of Birmingham, England.

Population Could Create a Devastating Global Slowdown")

{kind=link}