By Hung-Gay Fung & Jot Yau

This article discusses how offshore RMB markets help internationalize the renminbi in the global arenas of trade and investment. These offshore markets including the offshore currency and deposits, currency swap, and dim sum bond markets, enable the RMB to trade freely and allow market forces to play a role in the internationalization of the RMB, setting the stage for the RMB to become fully convertible. These offshore markets promote the use and circulation of the RMB outside China.

Dim Sum Bonds

The ‘dim sum bond’ market is an offshore debt capital market for bonds denominated in the Chinese currency, i.e., the renminbi or RMB.1 Coupled with other renminbi offshore markets such as the RMB currency swap and deposit markets, the dim sum bond market plays a pivotal role in the internationalization of the renminbi and in the pricing of its value. Although recently there have been some dim sum bond activities in London and Singapore, the dim sum bond market based in Hong Kong is unequivocally the leader in this offshore debt market. The Hong Kong dim sum bond market has benefited significantly from being based in Hong Kong where the first offshore RMB deposit center and the primary offshore trade settlement center for RMB trade transactions were established.2

Since its inception in 2007 till mid-December in 2012, the dim sum bond market has issued 780 bonds for RMB396.9 billion or US$63.8 billion (Table 1). In general, dim sum bonds have relatively short tenor (averaged 2 years), smaller and declining deal size (averaged RMB508.84 million or US$81.75 million), and higher coupon (averaged 2.8%) than the onshore RMB-denominated bonds in mainland China. The dim sum bond market experienced a run-up in volume in 2011 when the Chinese government liberalized policies regarding the offshore RMB debt financing. In addition, new policy initiatives that aimed at supporting the renminbi to become a global reserve currency also helped boost the growth in the dim sum bond market.[ppw id=”82517989″ description=”” price=”0.70″]

Several factors have fostered the development of the dim sum bond market. First, the relentless efforts of the Chinese government to set up and promote an offshore RMB-denominated debt market are instrumental to the growth of the dim sum bond market. As the Chinese government strives to internationalize the renminbi, the dim sum bond market is part of the grand scheme that includes establishing an offshore RMB deposit center, a currency trading center, and a currency swap market, among other initiatives. In particular, the large pool of the offshore renminbi deposits in Hong Kong has created a natural demand for dim sum bonds. Second, the 2007-2008 global financial crisis and the European fiscal crisis have provided significant impetus to the growth of the dim sum bond market as global investors were turned away from the US and European markets, looking to China, particularly the dim sum bond market, for alternatives. China has remained to be one of the major markets that still enjoy some growth momentum in the wake of the global economic slowdown, rendering dim sum bonds an attractive asset for investment. Finally, the renminbi has appreciated quite significantly against the US dollar since the issuance of the first dim sum bonds, enhancing the return on the dim sum bond investments. Since 2005, the renminbi had appreciated 30% against the US dollar after the Chinese central bank abandoned the peg to the US dollar (see Figure 1 ).

As the dim sum market continues to evolve, it raises a tough but fair question. Is the growth of the dim sum bond market secular and sustainable? Given China’s long-term national policy of internationalizing the renminbi (such as the trade settlement and currency swap policy) and the growing size in the offshore renminbi deposits in Hong Kong as well as in other potential centers like London, Singapore, New York, and Taipei, it is reasonable to expect a sustainable upward trajectory in the growth of the dim sum bond market as it further develops into a global market.

Offshore RMB Deposits

The growth of RMB deposits in Hong Kong reflects the impact of the changes of the Chinese government policy on the RMB over time. The total RMB deposits had grown from RMB33.4bn at the end of 2007 to RMB571bn by the end of November 2012, while the number of authorized financial institutions that are allowed to engage in RMB business increased from 37 to 138 over the same period.3 In addition, London, Singapore, New York, and Taipei have also begun to accumulate small pools of RMB deposits.

The growth in offshore RMB deposits in Hong Kong is largely due to two factors: the investor expectation of RMB appreciation against the US dollar and the rapid growth in the use of renminbi in trade and investment settlement. Many Hong Kong residents parked their cash in RMB deposit accounts at local banks for quite some time before 2007, hoping to benefit from the expected appreciation of the Chinese currency against the Hong Kong dollar, which is pegged to the US dollar. RMB deposits are now approximately 8.75 percent of the total deposits in Hong Kong4 and we expect it to grow over the next few years as the offshore currency market develops and more investment conduits become available as part of the national liberalization policy.

Although the slowdown of the RMB appreciation in the last quarter of 2011 reversed the upward trajectory of RMB deposits in Hong Kong for almost a year, it appears that the volume of RMB deposits had bounced back in November 2012. HSBC recently forecast that the renminbi deposits will account for 30% of the total bank deposits in Hong Kong by 2015.5 If the forecast is correct and with this RMB deposit base as the foundation, the pivotal role of Hong Kong in helping China to internationalize the RMB and to make it a global reserve currency that rivals the US dollar will continue.

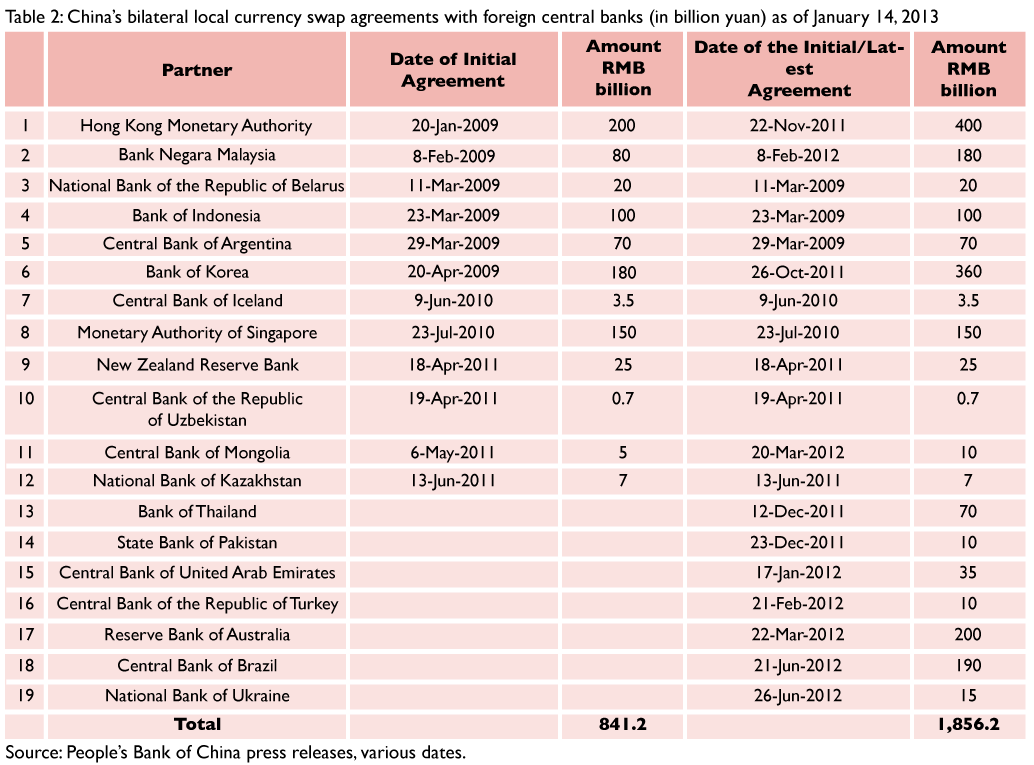

Currency Swaps

The rise in RMB’s value relative to the US dollar in early 2008 caused many Chinese exporters to go bankrupt, who got less RMB for each dollar they received. The ability to settle trade in RMB would reduce this exchange risk to Chinese businesses. Bilateral local currency swap agreements were set up between the Chinese and foreign central banks to mitigate the foreign exchange risk. The swap agreement permits the foreign central banks to sell RMB to local buyers who want to purchase Chinese goods and services and swap their own currencies for RMB with the Chinese central bank. This is particularly useful for foreign importers struggling to obtain trade financing in RMB in the wake of the financial crisis. The swap agreement may be applied to settlement for foreign investments.

Table 2 lists China’s bilateral local currency swap agreements with other countries. The agreement with Hong Kong registers the largest amount (RMB400bn), followed by agreements with Korea (RMB360bn), Australia (RMB200bn), Brazil (RMB190bn), and Malaysia (RMB180bn). These amounts reflect the country’s relative importance in trade with China. The total agreed amount is now over RMB1.8 trillion, which does not include the direct currency trading between the Japanese yen and the renminbi, which was started in June 2012. The increasing number of the bilateral local currency swap agreements with trading partners as well as the direct currency trading of yen-RMB indicates the Chinese government’s unequivocal commitment to the internationalization of the RMB.

Offshore Currency Trading

Global trading in RMB allows businesses to buy and sell the currency to finance trade, investment, and borrowing. Since 75 percent of China’s RMB trade settlement is done in Hong Kong, Hong Kong has played a major role in offshore RMB trading, having a daily turnover of around RMB1.5-2 billion.6 The Chinese authorities broadened the scope of the RMB trading program in December 2010 by increasing the number of qualified exporters from a few hundred to nearly 70,000 who could use the RMB in paying for their goods. Some suggest that the currency trading in RMB will increase to a magnitude of US$2 trillion equivalent worth of transactions per year by 2015 when half of China’s trade with the emerging markets settles in RMB7. Compared to the US$4 trillion daily trading in the global currency market, trading in the RMB is dwarfed by trading in the US dollar, yen and euro. However, RMB’s offshore trading has been impressive because of its speedy gain in trading volume. Moreover, Singapore, London, New York, and Taiwan are now poised to trade offshore RMB, adding more activities to the total volume.

More significantly, as pointed out above is the direct trading in yen-yuan, which began in June 2012. Since China and Japan are among the largest economies in the world, direct trading of their currencies boost trade and investment as well as providing an impetus to enabling the renminbi to become a truly global currency. The direct trading will lower transaction costs and reduce settlement risks of the financial institutions, saving the two countries some 3 billion dollars of transactions costs annually.8 Trade between China and Japan hit a record high of 344.9 billion US dollars in 2011, with only less than 1 percent of it settled in RMB and most of it settled in the US dollar.9 Direct trading will add volume to RMB offshore trading and Tokyo will likely become a RMB offshore center.

Trade settlement

Since February 2004, banks in Hong Kong could offer limited RMB-denominated banking services to Hong Kong residents and specified business customers. In July 2009, participating banks in Hong Kong were permitted to engage in the settlement of RMB trade transactions under a pilot scheme, which was extended in June 2010 to cover twenty provinces and cities in China as well as making RMB trade and other current account item settlement available in all countries. In 2010, trade settlement in RMB was just 2.5% of China’s total trade, whereas in 2011 it exceeded RMB2 trillion or $318 billion, 10% of China’s total trade.10

While RMB trading centers may geographically scatter around the world, popular adoption of the RMB for trade settlement will significantly increase the demand for RMB.

Developments in Other Markets

Several developments across markets (London, Singapore, New York, and Taiwan) related to dim sum bonds are noteworthy. London has jumpstarted its offshore RMB center status by issuing the first dim sum bonds outside Hong Kong. It potentially can be a successful offshore RMB center since it can tap the RMB businesses in European countries. It also has the advantage of being a world financial center, having first-class financial industry infrastructure like New York City. Singapore, a long-time rival to Hong Kong in the race as the leading world financial center in Asia, has niches similar to London or New York City. The Singapore Exchange (SGX) has clearly signaled its ambition to capture a slice of the trading business in securities denominated in renminbi, announcing its wishes to list, quote, trade, clear, and settle securities denominated in RMB. SGX have already listed offshore renminbi bonds and has also been the first exchange to offer the clearing of over-the-counter foreign exchange forward contracts in renminbi.11 New York City (NYC) would make an excellent offshore renminbi hub for several reasons including its financial industry infrastructure, geographic location, and trade and economic ties with China.12 These reasons suggest that NYC could easily generate substantial renminbi deposits and connect the renminbi business for banks that have RMB clearing arrangements with other global financial centers.

Taiwan is a latecomer to the offshore RMB market. Recent developments include the opening up of a branch in Taipei by the Bank of China in June 2012, making it the first Chinese mainland bank to start commercial operations and provide renminbi settlement services in Taiwan. In addition, Bank of Communications, the fifth largest Chinese bank in mainland China, has also been approved by Taiwan authorities to open its branch in Taipei. Likewise, the Chinese authorities have also approved ten Taiwanese banks to set up branches on the mainland, of which at least eight have already opened their branches.13 The growing RMB business between Taiwan and China will help sustain the offshore RMB business for China.

Concluding remarks

This article outlines existing and future forces that support the development of the dim sum bond market, which is part of the RMB internationalization process. In light of the relentless support by the Chinese government to internationalize the renminbi, the dim sum bond market is likely to grow. While RMB trading centers may geographically scatter around the world, from Singapore, London, New York, to Taipei, popular adoption of the RMB for trade settlement will significantly increase the demand for RMB.

Moreover, the revised Renminbi Qualified Foreign Institutional Investor (RQFII) program enables the QFII to invest the RMB raised outside of China (e.g., from the dim sum bond market) in Chinese equities, a step further strengthening the growth of the dim sum bond market. Under the revised program as of November 2012, the China Securities Regulatory Commission, the People’s Bank of China, and the State Administration of Foreign Exchange agreed to increase the quota for the program to $32 billion from just over $11 billion, thus increasing the demand for RMB.14 Thus, the growth of the dim sum bond market will help increase the supply of, and demand for, the renminbi and hence the RMB’s liquidity. As China plays a greater role in the global economy, the renminbi will be poised to become a global reserve currency in the future.

As the offshore renminbi markets open up to international investors, free market forces will take its toll on two offshore renminbi markets that are dependent on the inconvertibility of the RMB. One is the synthetic RMB-denominated bond market that requires interest payments in US dollars.15 If the currency swap market for dim sum bonds is fully developed, the synthetic dim sum bonds will no longer appeal to investors. The other market is the non-delivery RMB forward contracts, a popular hedging instrument for the renminbi traded in Hong Kong and Singapore.16 As RMB becomes more accessible and widely used, this market is likely to disappear. In addition, demand for products from these two markets is likely to decline as substitutes such as the RMB futures contracts are now available at the Hong Kong Exchanges and CME.17

Last but not least, the long-term outlook of the dim sum bond market is cautiously optimistic even if the RMB internationalization process completes or is close to complete faster than expected. If the Eurodollar or Asian dollar market was of any guide to the onshore US dollar markets, it may suggest that the dim sum bond market could stay on even after the renminbi becomes fully convertible. The development of the Eurodollar bond market has been strong and continued to be sustainable even today after the barriers to capital flows created by the 1963 Interest Equalization Tax Law was removed. Given the Chinese government’s determination to make the renminbi a global reserve currency, we do not anticipate the dim sum bond market to wane and disappear soon.

References

1. Strictly speaking, the dim sum bond market should be called the dim sum debt market since its products include the short-term as well as long-term fixed income products. We follow the convention to call this segment of the debt capital market the dim sum bond market. See Fung, Hung-Gay, Glenn Chi-Wo Ko, and Jot Yau, “Dim Sum Bonds – The Chinese Offshore RMB-Denominated Bonds,” Working paper, University of Missouri, St. Louis, and Seattle University, January 2013.

2. See Fung, Hung-Gay, Jr-Ya Wu, and Jot Yau, “Recent Policy Changes Toward the Internationalization of the Renminbi: A Review,” Chinese Economy, forthcoming, 2013.

3. Source: HKMA

4. As of November 2012, computed by authors according to deposit statistics from HKMA.

5. “Ready for the RMB?” Week in China, Autumn 2012, p. 3. Assessed at www.weekinchina.com on January 12, 2013.

6. Chien Mi Wong, “CME extends maturity of CNH futures,” AsiaMoney, September 21, 2012, (updated September 25). Assessed at http://www.asiamoney,com/article/3091746.

7. Carnevale, Francesca, “The game changer: Dim sum market sets new pace for RMB acceptances,” FTSE Global Markets, October 2011, p.10.

8. Lu Hui, “China starts direct currency trading with Japan,” English.news.cn June 4, 2012 assessed at news.xinhuanet.com.

9. Ibid.

10. “Shanghai Cracks Door Open For Hedge Funds,” Wall Street Journal, April 2, 2012.

11. See “SGX seeks a slice of RMB securities markets,” Financial Times, July 6, 2012. http://www.ft.com/intl/cms/s/0/c81aa310-c71e-11e1-943a-00144feabdc0.html#axzz2EfwbtD00

12. Fung, Hung-Gay, Jr-Ya Wu, and Jot Yau , 2013, “Recent policy changes toward the internationalization of the renminbi: A review,” Chinese Economy, forthcoming.

13. See http://www.china.org.cn/business/2012-06/28/content_25754896.htm

14. http://www.benzinga.com/trading-ideas/long-ideas/12/11/3081025/chinas-increased-rqfii-quota-could-lift-this-etf

15. For the description of the synthetic RMB-denominated bonds, please see Fung, Hung-Gay and Jot Yau, 2012. “The Chinese Offshore Renminbi Currency and Bond Markets: The Role of Hong Kong,” China and World Economy, 20(3), 107-122.

16. Fung, H-G., W.K. Leung, and J. Zhu, 2004, “Nondelivery forward market for Chinese RMB: A first look,” China Economic Review 15, 348-352.

17. The Hong Kong Exchanges (HKEx) introduced the renminbi (RMB) currency futures on Sept. 17, 2012. The U.S. dollar (USD) versus RMB traded in the Hong Kong contract is the world’s first deliverable RMB currency futures with maturity less than one year. The CME Group is scheduled to launch on February 25, 2013 its own USD/CNH futures. The CME USD/CNH futures contract has a standard contract size of US$100,000 and E-micro size of US$10,000 with a three-year maturity will also be physically delivered. See Financial Times, September 13, 2012. Assessed at http://www.ft.com/cms/s/0/280c8690-fd74-11e1-8e36-00144feabdc0.html#axzz2EP2swcr7 (“CME Group to launch renminbi futures”)

[/ppw]

About the Authors

Hung-Gay Fung is Dr. Y.S. Tsiang Chair professor at the College of Business Administration and Center for International Studies, University of Missouri-St. Louis, where he is also the head of the finance department. Jot Yau, CFA is Dr. Khalil Dibee Endowed Chair in Finance at the Albers School of Business and Economics, Seattle University, where he has served as the chair of the department of finance and MSF program director. He co-founded Strategic Options Investment Advisors Ltd., a Hong Kong-based investment advisory firm.

Population Could Create a Devastating Global Slowdown")

{kind=link}